The essence of strategy is choosing what not to do.

The private dining room at Durant’s had the kind of warmth that came from dark wood, low light, and fifty years of beef fat seasoning the air. Sarah had chosen the restaurant deliberately. Durant’s was old Phoenix, the steakhouse where real estate developers closed deals and trial lawyers celebrated verdicts. It projected seriousness without pretension, which was exactly the tone she wanted for the first in-person board dinner since Margaret Adeyemi had joined. It was the first week of October 2027.

The table was set for four. Alex Hawthorne sat to Sarah’s left, sleeves rolled to the forearms the way he always wore them when he was off-duty, a glass of Tempranillo already half gone. Across from him, David Park had his Moleskine closed for once, a concession to the social nature of the evening. And at the far end, Margaret Adeyemi studied the menu with the focused attention of someone who brought the same rigor to ordering a steak as she did to reviewing a board deck.

Margaret was sixty-one, tall and angular, with close-cropped silver hair and reading glasses she wore on a thin gold chain. She had spent the better part of thirty years as a general counsel, first at a Fortune 500 manufacturer, then at a healthcare conglomerate where she had overseen three acquisitions and one divestiture. Alex had recruited her to the board roughly a year earlier, in the fall of 2026, telling Sarah that Margaret would be the person who asked the questions no one else would think to ask. He had been right. Over the board meetings she had attended by video, Margaret had identified a client concentration risk Sarah had been ignoring and pushed for the quality governance framework that was now part of the organizational roadmap.

This was their first dinner in person. Sarah had spent two hours that afternoon preparing a summary of the numbers: $3.5 million run rate, EBITDA margins at 34 percent and trending toward 40, sixteen active clients, Tom Kaufman’s new subscription and the Cascade Biologics referral just signed, the recurring book deepening. The best quarter Candor had ever posted. She had the deck on her phone but hoped she would not need it.

“These are excellent numbers,” Alex said after Sarah walked through the highlights over appetizers. “Genuinely excellent. Not just for where you are, for any professional services firm at this stage.”

“The EBITDA trajectory is what interests me,” Margaret said. She had barely touched her salad. “You are at 34 percent blended. Where does that go?”

“Thirty-eight percent by end of Q2 if the Standardize volume holds,” David said. “Forty percent is achievable by Q3 if we add two more subscription clients at the Meridian tier.”

Margaret set down her fork. “Client concentration. You have sixteen clients, but what percentage of revenue comes from the top three?”

Sarah felt the familiar tightness in her chest that Margaret’s questions always produced. “Forty-one percent.”

“That is too high. If Tom Kaufman leaves again—”

“He is not leaving again,” Sarah briefly interjected.

“You do not know that. No one ever knows that.” Margaret’s voice was not unkind, but it carried the weight of someone who had seen relationships evaporate for reasons that had nothing to do with service quality. “What is your pipeline conversion rate?”

“Twenty-two percent of qualified leads convert to engagements,” David said. “Up from sixteen percent six months ago.”

“Good. But twenty-two percent means seventy-eight percent say no. Do you know why they say no?”

Sarah opened her mouth to answer, but Alex raised a hand. The gesture was subtle, a half-lift of the palm.

“I want to shift the conversation,” he said. “Sarah, everything Margaret is asking matters, and we should come back to it. But I want to put something on the table that I have been thinking about for a few weeks.”

He took a sip of wine and set the glass down with the deliberateness that Sarah had learned meant he was about to say something he had rehearsed.

“You have built something that works. The model is proven. Not hypothetically, proven with real clients, real revenue, real margins. The next question is not whether to grow. It is how. And I think the answer is: find the firms on the wrong side of this ‘AI enlightenment,’ acquire them and put them on the path to quasi tech multiple.”

The word hung in the air. Acquire. Sarah had been prepared for this dinner to be about Series A timing (when to raise, how much, at what valuation). She had not been prepared for acquisitions.

David reached into his jacket and pulled out his Moleskine. He opened it to a clean page. He was a creature of habit and simply could not help himself.

Margaret removed her reading glasses and let them hang on their chain. “Alex, before we go there, Sarah, have you thought about what kind of firm you want to be in five years? Because building from scratch versus combining can lead to very different places.”

Sarah looked at Margaret, then at Alex, then at the untouched bread basket between them. She had thought about what kind of firm she wanted to be. She thought about it constantly. But she had never framed the question in those terms, two paths, each leading somewhere entirely different.

“I think,” Sarah said carefully, “that is exactly the right question. And I think I need to answer it before we talk about anything else.”

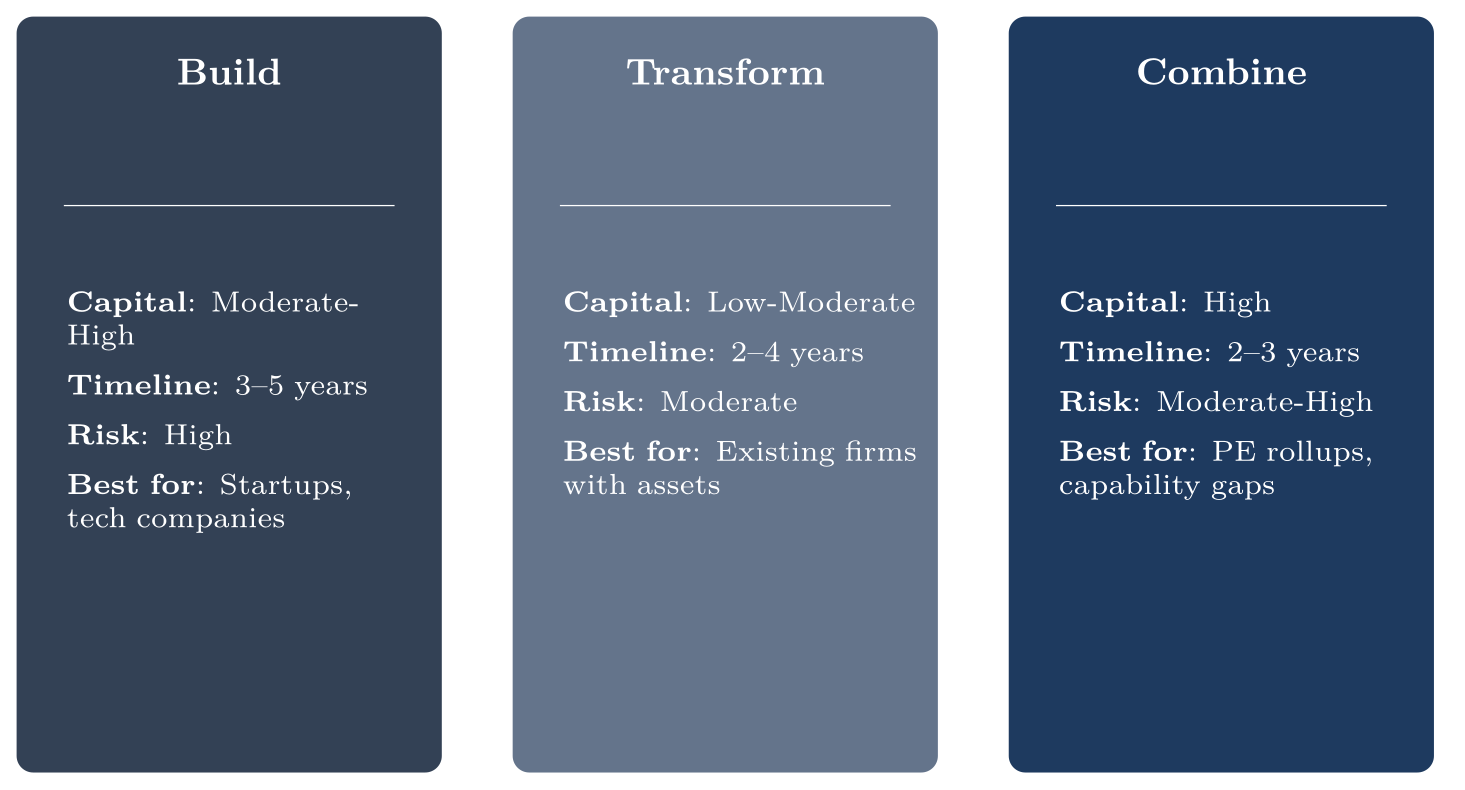

Candor’s journey addressed the dimensions of transformation (strategy, services, organization, technology, clients, and talent). But it did not address the fundamental question: How do you get there?

Three paths lead to AI-native professional services operations:

These are the paths that can define transformation for various organizations. Each path has advantages, disadvantages, and risks. Candor was, of course, already executing the Build strategy. The question was whether they might pair this effort with a combination led strategy.

Sarah arrived at the office at 6:15 the next morning, an hour before anyone else. The building was quiet, the particular quiet of a Friday before the phones started ringing, when the HVAC system hummed and the coffee machine gurgled through its first cycle. She poured a cup, black, and sat at her desk with the dashboard open on one monitor and a yellow legal pad in front of her.

She wrote three words across the top of the pad, each underlined:

Build. Transform. Combine.

Under Build, she wrote: I have done this. Three years of it. From nothing to $3.5M.

Under Transform, she wrote: This is what our clients need. This is what our competitors might do. Easier said than done.

Under Combine, she wrote: This is what Alex wants. Buy a firm, absorb their clients, double revenue.

She stared at the three columns. The original business plan (the one she had written on her laptop in a coffee shop three years ago, the one that had convinced Alex to write the first check) had been entirely about Build. Start from zero. Hire the best people. Build the platform. Win clients one at a time. Prove the economics. The plan had said nothing about acquisitions because the plan had been written by a founder who did not yet know what she did not know.

Three years later, she knew more. She knew what Build had cost her: the sleepless months, the cash flow crises David papered over with spreadsheet gymnastics, the Joshua Thornton disaster that had nearly broken the culture before it was formed. She knew that Build was slow, that it tested your stamina more than your intelligence, and that it worked only if you had the discipline to stay patient when every instinct screamed to move faster.

She also knew what Transform looked like from the inside, because she watched her clients try to go through it. Mid-market companies with legacy processes and resistant middle managers and technology stacks held together with duct tape and habit. Transformation was harder than building because you had to dismantle something while it was still running. “It was like rebuilding an engine while the car was still speeding down the highway.”

And Combine: she had never done it. Had never acquired anything. Had never integrated two organizations with different cultures, different systems, different assumptions about how work should be done. The prospect was exciting in the way that standing at the edge of a cliff was exciting: the view was extraordinary, and the consequences of a misstep were permanent.

She grabbed her pen and wrote one more line at the bottom of the pad: Which path leads to the firm I actually want? What will provide the most robust results for my stakeholders?

The Wrong Side of the Enlightenment

Sarah needed to understand what each path actually entailed before she could choose. Build, Transform, and Combine each ask a different question of a founder (or “intrapreneur” within an existing organization): whether you can attract the talent, capital, and clients to start from zero; whether you can change an existing firm fast enough while preserving what makes it valuable; or whether you can integrate effectively enough to capture the benefits of combination without inheriting the liabilities.

Sarah spent that evening scoring Candor on a variety of dimensions. Current Position: strong. Strategic Intent: aggressive growth. Time Horizon: moderate. Risk Tolerance: moderate-high. Partnership Consensus: not applicable (she was the founder, not a committee). She worked through the columns methodically and stopped at Resources Available. Capital: limited. Integration team: nonexistent. She circled the score twice. Candor was strong on nearly every dimension except the one that mattered most for a combine play.

Her phone buzzed. A text from David: Cascade scope expansion confirmed. $120K initial, $800K pipeline. Tom Kaufman is my favorite person ever. The build path was working. The question was whether it was working fast enough.

The following Tuesday, Alex sent Sarah a link to a video call with a one-line message: Found something. Tuesday 2pm your time.

Sarah joined the call from her office. Alex was in his home study in Los Altos, the bookshelves behind him lined with the biographies and business histories he consumed in bulk. David sat across from Sarah, anxiously awaiting what Alex had to say.

“Hargrove and Lyle,” Alex said. “Twelve-lawyer firm in Tucson. Regulatory compliance and commercial contracts. Three key partners, two over sixty. Revenue steady at $4.2 million for the last five years, flat as a table. Zero AI. Zero innovation. Basically, it was a firm born of the 1980’s largely untouched by time. Two of the partners want to retire within eighteen months. The third, Janet Hargrove, is fifty-eight and still has energy to push on. She is the one who keeps the lights on.”

“How do you know about them?” Sarah asked.

“A friend at a PE fund looked at them and passed. Too small for their model. But the profile is perfect for you.” Alex leaned forward. “Their clients are your clients, mid-market companies with regulatory compliance needs. Port their book onto your platform, cross-train their lawyers, double your revenue in six months.”

David was writing. Sarah could see the letters from across the desk: H&L — 12 lawyers, $4.2M, flat 5 yrs, 0 AI.

“What would an acquisition look like?” David asked.

“The two retiring partners want a clean exit, buyout of their equity, maybe an earn-out tied to client retention. Janet would stay. Some of their associates might work in an AI-native model. Some obviously won’t.” Alex paused. “I think you could do this for $5 to $6 million. Structure it with a significant earn-out so the upfront cash is manageable.”

Sarah leaned closer to the screen. The numbers were attractive. Twelve lawyers, thirty-two clients, a regulatory practice that overlapped almost perfectly with Candor’s core competency. If even half of the client relationships survived the transition, it would add more than $2 million in annual revenue. Combined with the existing run rate, Candor would be $5.5 million or perhaps upwards of $6M. That was Series A territory. That was a real firm.

But.

After the call, she picked up the phone and dialed Maya Feldman. Maya answered on the second ring, the sound of Manhattan traffic in the background.

“Alex wants me to acquire a firm,” Sarah said.

“Tell me about it.”

Sarah described Hargrove & Lyle: the profile, the numbers, the strategic logic.

Maya was quiet for a moment. “Every acquirer thinks they are buying clients and talent. What they are actually buying is culture, and culture is the thing that breaks in integration. What is their culture?”

“Traditional. Twelve lawyers, three senior partners, hourly billing, paper-heavy processes.”

“So the opposite of everything you have built.”

“Alex says the clients are the asset, not the culture.”

“Alex may be right about the strategic logic. I have seen acquisitions work, but rarely at this stage, and never without a dedicated integration team in place before the deal closes. You do not have that person. You barely have an operations lead who is not already running everything else.” Maya paused, and Sarah could hear her thinking through the next piece. “The clients stay because of the culture: because they know the partners, because they trust how things are done. You change the culture, you risk the clients. That is the part nobody can quantify in a spreadsheet, and it is the part that breaks.”

“So you think it is a bad idea.”

“I think it is a real idea. That is what makes it dangerous. If it were obviously bad, you would not be calling me.”

Sarah felt the tension between Maya’s caution and Alex’s conviction settle in her head. “Listen Sarah, it is all about the earn out here. It would need to be tiered and spread over time with payouts tied to client retention at the one and two year anniversary. If they cannot help you transition the clients then the entity has no independent economic value. It is as simple as that. Whether they will accept that reality, however, is another story.” She thanked Maya and hung up.

Twenty minutes later, an email arrived from Margaret Adeyemi. No subject line. The body read: Sarah, I have seen twenty acquisitions in my career. Three worked well. Five were acceptable. The rest destroyed value. The difference was always integration discipline, not deal price. Be careful. —M

Greenfield or Brownfield Development

Starting from Zero

The build path is the one Sarah has actually walked, and the one she had been quietly comparing herself against ever since the well-capitalized AI-native cohort started showing up in 2025 with venture rounds north of $50 million. The argument for building is real. A firm started from zero carries no legacy partnership agreement to renegotiate, no legacy document management system to migrate off of, no senior partners who built their books on hourly billing and would prefer to retire before that changes. Sarah designed Candor’s pipeline around verification from the first engagement. She hired Priya specifically to build the platform Candor needed rather than to integrate the platform Candor had inherited. The structural flexibility was real too. She chose her entity form, her fee model, and her staffing ratios without anyone’s permission.

The cost of starting from zero is the cost Sarah has already paid and is still paying. No existing clients meant every dollar of Candor’s first $3.5 million in revenue had to be earned from a buyer who had never heard of the firm. The Tom Kaufman relationship that became foundational started with a conference panel and a near-disaster on the Meridian engagement. No brand meant general counsel had to be convinced that an unknown Phoenix firm could handle work their incumbents had been doing for fifteen years. No track record meant Margaret Adeyemi’s first investment thesis rested almost entirely on the team and the platform, because the operating history did not yet exist. The capital burn was real: Candor’s seed round funded the J-curve dynamics described in Chapter 2. It had to spend to build rather than just buying revenue from a weakened gazelle on open savanna.

The high-velocity AI-native startups of 2025 and 2026 chose a different version of the same path. They raised $50–100+ million up front, often as technology companies first and law firms second, and used that capital to fund Arizona ABS or MSO style structures, proprietary AI platforms, and acquisitions of traditional practices that helped accelerate their path to revenue. Their build was capital-aggressive in a way Sarah’s was not. Her build was capital-disciplined in a way theirs could not afford to be. Both are build paths. The success rates for either version are far from 100 percent, and the capital requirements run from Sarah’s lower million trajectory to the $100 million-plus rounds the venture-backed cohort has assembled. Build when you have the capital, a differentiated platform, and a market where speed and structural freedom matter more than incumbent relationships. Don’t build when those relationships are exactly what you have and would be abandoning.

Cautionary Predecessors: Clearspire and Atrium

They say that “history doesn’t repeat itself but it often rhymes.” And history is littered with startup entrants who thought they might be able to fundamentally recast the legal services delivery model. So far they haven’t. The legacy model remains (almost entirely) intact. Clearspire (2011–2014) and Atrium (2017–2020) are the two most prominent and recent cautionary examples Sarah encountered when she was working up the courage to leave her firm. These entities were, in part, victims of timing. For both, the underlying AI systems were not yet sufficiently capable of fundamentally altering the unit economics of legal service delivery. The millions in venture funding which flowed to these entities produced growth expectations which an otherwise linearly oriented service business could not satisfy. Both firms had elements of the thesis right but the technology simply was not there (yet). These two predecessors offer lessons to anyone choosing the build path today, including the well-capitalized AI-native cohort that arrived in 2025 and the founders, like Sarah, who arrived earlier and on less capital.

These entities and others like them offer three major lessons. The first is that capital does not substitute for product-market fit. If anything, it hides the absence of fit until the runway runs out. Atrium’s $75 million was not an asset, it was an obligation, and the obligation outpaced the firm’s ability to deliver economics that justified it. Build-path founders raising at the venture multiples this generation has commanded should ask whether their unit economics could survive a flat year, because if the answer is no, the capital itself becomes the timeline pressure that breaks the build. The second lesson is professional identity. Clearspire hired former AmLaw 200 attorneys but marketed itself primarily as a technology platform. Atrium was founded by a technologist but lacked both the killer technology and the form factor that most buyers at that time were seeking. Today’s AI-native build firms get this right (Sarah is a lawyer running a law firm, not a technologist running a platform), and the firms that do not get this right might end up as the surviving ALSPs ended up: semi-profitable (at best) in narrow low stakes niches, but never truly invited to the advisory table.

The third lesson is the one most relevant to the path selection decision in front of every legal services organization right now (including Candor). While the precise calculus might vary, each organization faces choices. That is true for Sarah. That is true for Marcus Chen. That is true for Hargrove & Lyle. It is true for every ALSP, AmLaw 200 firm, small firm and large firm as well. Vision is necessary but not sufficient for a build based strategy to work. The technology and the regulatory permission have to be available in the same window. If imitation is the sincerest form of flattery, then Clearspire’s two-entity structure, fixed-fee model, and operating discipline all look correct (seen in the eyes of today). However, in the case of Clearspire, the AI capability that would have really made the economics work was more than a decade away. Atrium’s investor base, sales motion, and growth ambition were all correct. However, the AI capabilities that would have justified the burn rate were still several years away.

Surgery on a Moving Patient

Transform is the question that almost every firm reading this book is facing, and almost no firm reading this book is Candor. The build path requires capital, regulatory freedom, and a willingness to start with no revenue, and the firms that have the appetite for those terms are a small minority. The overwhelming majority of law firms have the opposite profile: clients, talent, brand, and a partnership that took decades to assemble. That is the position in which Marcus Chen finds himself, and his Phoenix boardroom is where most readers will recognize themselves.

Marcus is, on paper, an unlikely candidate to lead a transformation initiative. He has spent eighteen years inside his firm, Stratton Hewitt & Calloway, building a regulatory practice the way the practice had always been built: hourly billing, partner relationships, the staffing pyramid. He is exactly the kind of senior partner who could try to ride that horse to retirement and let the next generation deal with what came after. But the losses at Pinnacle, Western Regional, and Riverview have him asking questions he had not planned to ask, and the legal pad on his desk has stopped tracking clients to call and started tracking things the firm does not yet know how to do. The moment and the man may need to come together, and the firm Marcus has spent his career inside may need him to lead it into an AI-enabled future it has not yet figured out how to occupy.

Transformation builds on assets the build firms would love to possess. Even though Stratton Hewitt already lost the Pinnacle relationship to Candor, it still had many other clients. The firm had a strong crop of associates, and the brand swung open doors that Sarah was still straining to pry loose. Stratton Hewitt does have some existing technology at use in the firm. Existing funds can support at least a degree of transformation but this does require a commitment. A transforming firm can absorb a year or two of below-trend margins if partners are willing. But this is a big “if.”

Existing firms have disadvantages as well. The Stratton Hewitt document platform was state of the art in the 2010s and is now a legacy system that any new verification layer must interoperate with. The compensation grid Stratton Hewitt had used for thirty years was designed for an hours-based economy, and Marcus is about to propose a multi-million dollar transformation initiative which would require partners to forgo profits in the short run in favor of some future state of tech enabled profitability.

The transformation question is less of a software problem and more of a partnership problem, and it is not clear how Marcus’s proposal will fare. The frozen middle, the partners senior enough to have stakes and junior enough to need another fifteen years of those stakes, is where transformation usually stalls. Rumored explorations of MSO structures by leading law firms happen precisely because internal funding hits a wall, and the firms looking at outside capital are doing so to fund transformation that partner distributions will not.

Transformation, done seriously, is a three-act play and Marcus is about to take his place on the big stage. The first six months are about building the case and securing leadership commitment, which is the act Marcus is performing in the Phoenix boardroom. The next six to twelve months are pilot: a contained domain, real metrics, stage gates that let the partnership pull the plug or double down. Marcus’s healthcare regulatory pilot is structured this way for reasons that have less to do with healthcare and more to do with what a partnership will tolerate when partner distributions are the funding source. The scale phase that follows, twelve to twenty-four more months, is where the compensation grid might actually be placed under real pressure. The firms that survive this phase likely share two characteristics: they kept the pilot short (long pilots are how dual operating systems become permanent), and they treated revenue pressure as a strategic problem rather than a budgeting one. Transform when the relationships are worth preserving, the leadership is genuinely committed, and the competitive runway is long enough to let the J-curve play out. Don’t transform when any of those three is missing, because the math does not survive their absence.

Sarah’s relationship to the transform question is different from Marcus’s, and it is worth highlighting the difference once again. Candor does not need to transform. There is no legacy compensation grid to renegotiate, no document management system to migrate off of, no frozen middle of partners who need fifteen more years of hourly distributions. The firm Sarah built three years ago was already structured around the verification layer that Marcus is trying to retrofit into Stratton Hewitt. That asymmetry creates two possibilities Marcus’s firm does not have. The first is that Candor could sell transformation services to firms like Stratton Hewitt, advisory work for traditional practices going AI-native, packaged as the operating playbook David built for Candor’s own pipeline. The market for that work is real and growing, but the people who can do it credibly are scarce. So there is a real possibility that Candor could, in the end, be acquired by a larger fish (think AmLaw 100 firm) that has the size to overcome its lack of AI strength. Large enough fish have the resources to potentially become strong fish as well. The second possibility is that Candor could become the predator and just acquire or combine with smaller traditional firms whose weaker AI capabilities make them vulnerable.

Suffice it to say, it is a complex and quickly evolving ecosystem where the fitness landscape may come to favor a different set of characteristics.

The Canary in the Coal Mine

Marcus Chen had spent nine years in the same fifteenth-floor office, the best in a series of rooms that had improved with every rung he climbed at the firm. Big window, north-facing, a partial view of Camelback Mountain when the haze cooperated. He liked the room when it was empty. Quiet, the floor mostly clear by six-fifteen, the lights dimmed to whatever the building’s automation thought was appropriate for an associate working late.

It was 6:47 on a Friday now in the third week of October 2027.

Marcus had a spreadsheet open and a yellow legal pad next to it.

The spreadsheet was the practice group’s quarterly pipeline. Won, in-progress, lost, and a column he had added himself last year called lost to whom. He had stopped trusting the firm’s standardized lost-to-whom values (Big Law, Regional, In-house, Other) because the answer that mattered most was hiding inside Other.

He scrolled to the lost section and counted again.

Three deals in the last six months. Three deals he could remember pitching. Three deals he had walked into expecting to win.

The first one was Pinnacle Federal Credit Union out of Boise, a $240,000 detailed fintech partnership review. They had been a Stratton Hewitt client for fourteen years. Marcus had presented in front of their board personally in 2019. They had given the work to a firm called Candor Legal in Phoenix that no one at Pinnacle had previously heard of. The follow-up call with Pinnacle’s general counsel, Trevor, had been gracious and precise. Marcus, your team has always done excellent work for us. The pricing model and the timing is what’s changed. They quoted us a fixed fee with a two-week SLA. Two weeks. And a fixed fee not an amorphous number of hours. I am sure you can appreciate the value of this as a client.

The second one was Western Regional Health, a vendor contract review project, two hundred agreements, the kind of work the practice group ran in its sleep. Marcus had quoted $47,000. Western Regional had gone with Candor at $22,000. The call had come only a few weeks ago, Jennifer Walsh telling him herself. She was polite but firm about the decision she had made. Different client. Same answer.

The third one was Riverview Mutual Bank out of Albuquerque, a $190,000 OCC examination preparation matter that Stratton Hewitt had handled annually for nine years. Riverview had used a competitor this year. Marcus didn’t know which one. He had spent a week trying to find out and had not gotten a satisfying answer.

Three in six months. $477,000 in lost revenue from three accounts the firm had treated as permanent.

Marcus picked up a pen and wrote a number on the legal pad: 477.

Then he wrote: out of how many?

He scrolled to the won column and added it up. The practice group had closed $4.2 million in new work over the same period. Lost-to-AI-native ran a little over ten percent of total addressable. Not yet a crisis. Not yet defensible to ignore.

477. Now he wrote: but next year?

He sat back. He had been a partner for eleven years, an equity partner for seven. He had watched the regulatory practice navigate 2008, the regional banking consolidation of 2014, the brief period after the 2020 election when the firm’s commercial litigators thought they were going to be busy and weren’t. Markets shifted. Clients moved. He had a calibrated sense of what panic looked like and what the absence of panic looked like, and the number on the pad was not yet panic.

But it was also something.

He closed the spreadsheet and pulled up a browser tab that had been sitting open since lunch.

Candor Legal’s website was unornate. A landing page with a tagline he did not fully understand (Verification, not just generation) and a navigation bar with four items: Services, How We Work, Metrics, Clients. He clicked Metrics.

The page that loaded contained, in plain numerical form, a set of operating disclosures Marcus’s firm did not publish to its own partners.

Average matter cycle time, twelve months trailing: 11.4 days.

Average error rate, post-verification: 0.3%.

Average client realization on fixed-fee engagements: 96%.

Net revenue retention, twelve months trailing: 138%.

He read the page twice and then opened the legal pad to a fresh sheet.

He had not taken notes on a competitor’s website in fifteen years. He had not, before tonight, considered Candor a competitor. He had considered them a curiosity. An experiment. A firm of unknown durability staffed by a former associate from another Phoenix firm.

He wrote at the top of the page: What are they actually doing?

He wrote: Fixed fee. Two-week turnaround. Published metrics.

He wrote: 96% realization. Mine is 84.

He underlined that line twice.

He wrote: Verification generation. What does this even mean?

He wrote: Net revenue retention 138%. They are not just winning new clients. They are growing inside existing ones.

He set the pen down.

Then he picked it up and wrote one more thing, in smaller letters, near the bottom of the page, as though he were not quite ready to commit it to the rest of the document.

I have been competing on what they can’t do. I am losing on what they can.

He underlined it once, considered it, and underlined it a second time.

His phone buzzed at 7:31. His daughter, Chloe, calling from Palo Alto. She was a 2L at Stanford Law working through the summer-associate decision he had been giving her advice on for three months. He let the call go to voicemail and called her back four minutes later, after he had put the legal pad in his briefcase. He gave her the same advice he had been giving her, which was to take the offer from the AmLaw firm with the strongest healthcare regulatory practice.

She listened. But she did not, this time, agree as quickly as she had the last two times that they had discussed it. She said the work she had been seeing at Stanford (the people, the technical projects, the ambient environment full of startups) had given her a different picture of what regulatory practice was going to look like in five years, and she was thinking about it.

He said he understood.

When she asked if he was at the office, he said yes.

When she asked if he was okay, he said yes.

He was, in some sense he could not yet articulate, not fully telling the truth.

The drive home took thirty-one minutes. He had timed it. He had timed it many times.

His wife, Linnea, was on the back patio with a glass of wine and the laptop she used for the gallery she had run for twenty-two years. She looked up when he came through the back door and noticed, the way she always noticed, that he was still carrying the legal pad.

“What did you find out?” she said.

He held the pad up.

“That if I had been doing what these AI native firms were doing for the last two years, we would still have Pinnacle. And Riverview. And Western Regional. And probably twenty other clients I haven’t lost yet — but might lose to them if we don’t get our act together.”

She looked at the pad for a moment.

“Are you going to tell the partners?”

“Yes.”

“Are they going to want to hear it?”

“Probably not.”

She closed the laptop.

“Tell me about it from the beginning,” she said.

He did.

The Acquirer’s Temptation

The traditional acquirer’s temptation was to overreach: to swallow a target the buyer could not digest, to confuse strategic logic with integration capacity, to mistake the seller’s revenue for the buyer’s future. The AI-native version of the temptation runs the opposite direction. The temptation is to wait. It is tempting to assume that a fifteen-lawyer firm with verification discipline cannot be the acquirer of a twelve-lawyer firm with thirty years of relationships. Traditional combination wisdom says you absorb up from below, not across. But this was the old world.

Unless the scales are radically different (e.g. boutique firm versus a magic circle firm), the headcount math is the wrong math. Sarah is the strong fish. Hargrove & Lyle is the weak fish. The relevant strength is not the partner roster, it is the AI capability that determines what a lawyer can deliver and what the work costs to produce. Tom Kaufman’s subscription, Cascade Biologics moving along, strong EBITDA margins, Candor OS 2.0 shipping quickly because Priya had built a team that could ship things quickly. These are the assets that determine who absorbs whom. A fifteen-person AI-native firm with verification discipline and real AI capability can absorb a twelve-lawyer traditional practice and produce more value from the combined book. The reverse is not true.

AI is the massively differentiating technology of this generation, the economic engine that decides which firms are strong notwithstanding their headcount. The operating leverage compounds where the partners-per-matter ratio does not. The frame inverts the prior decade of professional services M&A. The big-vs-small distinction that mattered in 2015 was headcount. The strong-vs-weak distinction that matters now is something like “AI capability per lawyer.”

That inversion is what Alex Hawthorne was selling Sarah at dinner. Hargrove & Lyle is $4.2 million in revenue with three named partners (two of them ready to retire) and client overlap that is almost too good. The strategic logic is real because the AI-strength gap is real: Candor can run Janet’s regulatory book at a fraction of Hargrove’s current cost structure and still deliver work that meets Janet’s clients’ expectations, because the verification layer does what eight Hargrove associates currently do, and the lawyers who remain spend their time on the judgment work that is actually scarce. The pattern is familiar to those with a broader understanding of the history of professional services and the economics thereof.

The healthcare MSO consolidators built nine-figure platforms on exactly this thesis: acquire fragmented incumbents, hold the clinical work inside the regulated entity, hold the operations and capital in the management company. They were the strong fish on operating capability long before they were the big fish on revenue.

As previously noted, combinations come in several shapes. An incumbent may acquire an AI-native entity (a platform, an ALSP, a specialist team) to leapfrog its own transformation timeline. An AI-native firm may go the other direction, as Sarah is being asked to consider, eating practices that traditional acquirers could not have made work because their cost structure could not have absorbed the target’s revenue. Two firms of similar size may merge. Private equity may buy a platform and bolt smaller firms onto it. Or the parties may stop short of full combination and build a joint venture, sharing technology or client access without merging the partnerships. Every version compresses time. Every version pays a premium for that compression. And every version inherits a culture, a compensation history, and a client base whose loyalty was built on the prior way of working.

These disadvantages are why the failure rates are not lower, and they are exactly the disadvantages that Maya and Margaret named. Integration is where deals die. Cultures clash, systems do not connect, and the people who were the actual asset (the senior partners with the client relationships) leave faster than the earn-out can hold them. The acquirer pays a premium that bakes in the seller’s risk reduction, and then absorbs the distraction tax: leadership attention going to integration instead of clients. Regulatory complexity is its own layer in professional services. Fee-sharing rules, ownership restrictions, and bar oversight vary by jurisdiction and can block or delay transactions that looked clean on paper. Maya Feldman’s warning to Sarah on the Hargrove call captures the part the spreadsheet does not: clients stay because of culture, and changing the culture is how acquirers lose the clients they thought they were buying. Seen in this light, Margaret Adeyemi’s three-out-of-twenty success rate sounded plausible. The strong-fish thesis explains why a fifteen-person firm should consider eating a twelve-person firm. It does not explain when. Combine when capability would take too long to build, integration capacity actually exists, and the cultural distance between the two firms is something the buyer has the bandwidth to manage. Don’t combine when integration capacity is the thing being assumed rather than the thing being demonstrated.

Micromotives and Macrobehavior

The boardroom on the seventeenth floor of the One North Central had a long table built for fourteen and a monitor on the long wall that the firm had installed in 2020 and had been told, more than once, was already obsolete. The building was the Phelps Dodge Tower to everyone at the firm. The owners had renamed it One North Central years ago but the name never stuck. On a Wednesday morning in early November, all fourteen seats were filled.

Mr. Calloway was on the screen. He was in Denver and rarely appeared in person for board meetings anymore. However, his name was on the letterhead and so his voice was important.

Marcus had been told by three different partners, in three different hallways over the previous ten days, that this was the version of the proposal that could pass. He had asked each of them to confirm a yes vote and each of them had said yes. He had stopped counting at eight. He needed ten.

He stood at the head of the table.

The deck on the monitor was nine slides. He had started, two weeks ago, with sixteen. He had cut six the previous Sunday and one more on the drive in this morning. The first slide was a single number: $477,000. The second was a list of three clients. The third was the sentence Ten percent of total addressable, trailing twelve months. Trajectory: twenty-five percent in twenty-four months if unchecked.

He walked through the deck in eleven minutes. He had practiced for nine.

The proposal, on slide seven, was to invest $2 million per year and a total of $4 million over twenty-four months. This would fund two Legal AI Engineers at $250K–$300K loaded each. Hire three Legal Quality Analysts. Build on top of the firm’s existing document review platform. Deploy a senior associate full-time to run point. And most of all create a sizable “token budget” to fund the increasing token consumption required of those interested in leveraging the frontier models.

Marcus proposed to run the pilot in the healthcare regulatory arena. Stage-gate at six, twelve, eighteen, and twenty-four months. Slide nine was a chart he had built himself, comparing realization and net revenue retention between Stratton Hewitt’s regulatory practice and four named AI-native firms whose published metrics he had been collecting for three weeks.

He stopped talking. He sat down.

The vibe in the room was hard to read at first. It was clear that no one wanted to be the first one to speak.

Then Calloway, on the screen, set down a coffee cup.

“Marcus. Before we vote. I want to ask one question.”

“Of course.”

“The pressure you’re describing, the ten percent number, it’s in regulatory. Energy isn’t seeing it. Real estate isn’t seeing it. Litigation isn’t seeing it. Tax isn’t seeing it.”

He paused. He was not, Marcus knew, performing the pause. He was thinking.

“Why are we funding your problem with our money?”

Marcus had prepared for the question. He had prepared three answers to it. He had practiced two of them out loud on the drive in.

He gave the first one. It was about leading indicators: that regulatory was a leading indicator for the rest of the practice groups, that the same pricing pressure was coming for energy, for real estate, for tax, that building the capability in one practice now was cheaper than buying it across five practices later.

Donna Aldred, from Albuquerque, supported him. “He’s right about that. We’re going to be having this conversation in energy in a year or two. The work in regulatory is the canary.”

Calloway nodded but was about to disagree.

“Donna. I respect your read. I want to be convinced. Show me the energy-industry analog. Show me the AI-native firm taking energy work from us. Show me the published metric. I’ll be the first to vote yes.”

He paused again.

“Four million is what we projected for the Houston satellite. Which, by the way, is the next item on our agenda. It is a significant amount and so we need to be careful here. I am not against the proposal. I want it to work. But it is coming out of partner distributions and it is going into one practice group’s capability build, and the firm owes itself a clear answer to the question of why this is a partnership-level capital allocation rather than a regulatory-group cost. We owe each other that answer before we vote.”

The room was quiet again.

Hewitt, who had been a partner for thirty-one years and a named partner for nineteen, looked at Marcus over reading glasses he did not really need to wear and said nothing.

Marcus looked at the room.

He could see, in the faces of two of the partners he had counted as yes votes, the small recalibration that happens when the framing of a question changes. Williams, from Salt Lake City, had picked up his pen. Tate, from Midland, had set his down.

He had eight. He had probably, at this moment, six or seven.

He did the math in his head and decided not to take the loss.

“These are fair questions. I don’t have the answer in the shape this proposal needs. Let me come back to the committee with a different framing. I think the question matters and I don’t think I have this exactly where I want it.”

Calloway, on the screen, did the smallest thing with his shoulders that, in nineteen years of working with him, Marcus had learned was his version of approval.

“I appreciate that, Marcus. I am not against this. I want it to be the right proposal. You know we want to make sure our firm is an AI market leader.”

The committee moved on to the next agenda item, which was the opening of a satellite office in Houston.

Marcus had to stay for the vote on Houston. But Marcus did not want to stay for that vote — he wanted to scream.

He walked back to the fifteenth floor and closed his door.

The legal pad from October was on his desk. He had carried it home and back five times since the night he had written competing on what they can’t do at the bottom.

He turned to a fresh page.

He wrote at the top: Different framing.

He underlined it.

Then he wrote, beneath it: Calloway’s question is the right question. Answer it.

A knock. Hewitt, in the doorway, leaning on the frame the way folks lean on doorframes when they are about to say something they wanted deniability about later.

“He’s not against you, Marcus.”

“I know.”

“He’s just cautious, maybe too cautious.”

Hewitt held up a hand before Marcus could comment, the way he did when he wanted the last word to be his.

“Find something he can vote yes on.”

He left.

Marcus sat with the legal pad for a long time. Then he crossed out Answer it and wrote in its place: Give him something he can vote yes on.

He would regroup and try again because this was too important to just push aside. This was indeed a canary in the coal mine.

Six Columns on a Whiteboard

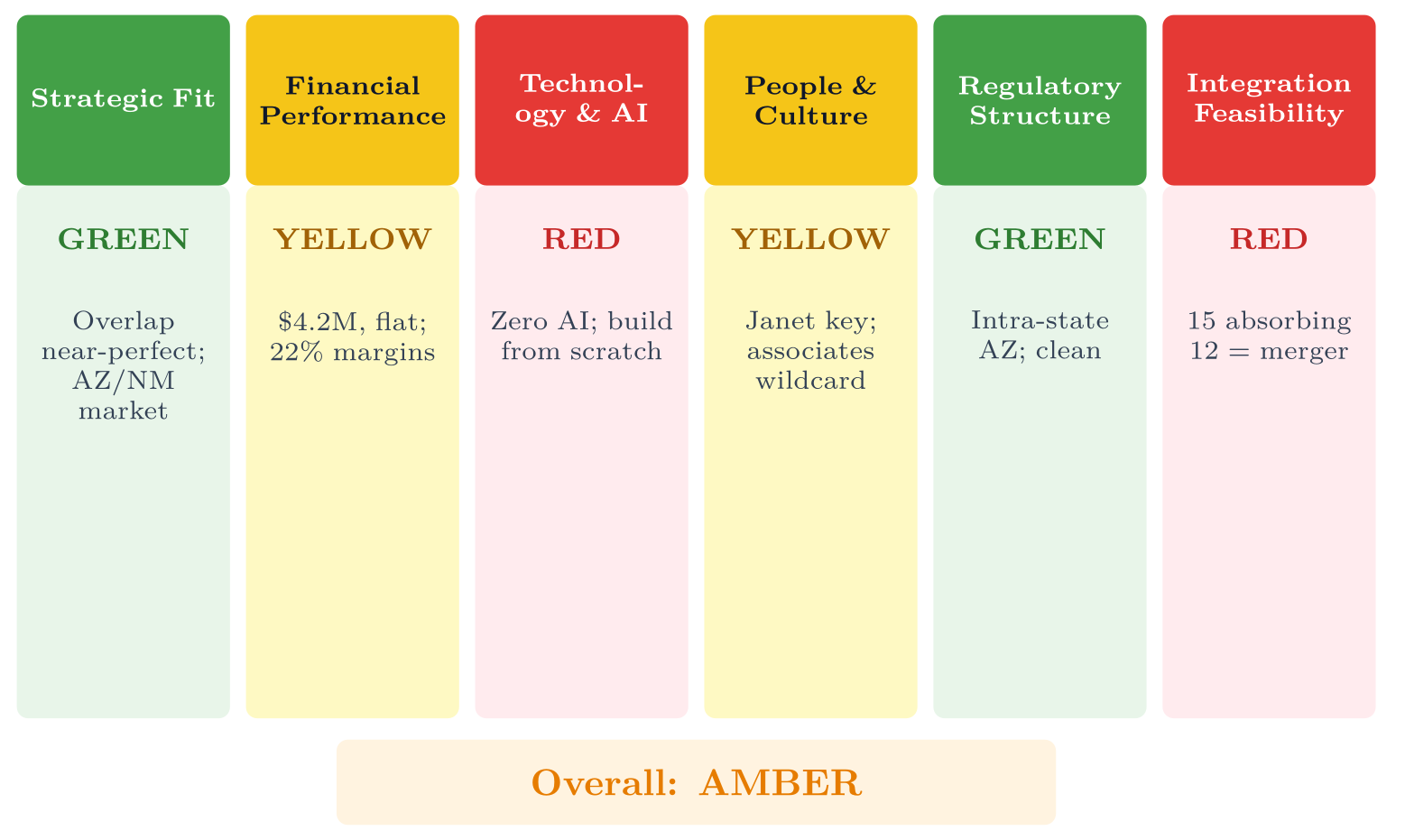

David had built an evaluation framework for any acquisition Candor might consider. He drew six columns on the whiteboard.

Saturday morning. Sarah had not planned to come in, but David had texted at seven: I have been running the numbers on H&L. Come look at the whiteboard.

She found him in the conference room with two coffees and the whiteboard covered in his precise block lettering. He had drawn six columns across the top (the M&A evaluation criteria) and was scoring Hargrove & Lyle against each one.

“Walk me through it,” she said, pulling up a chair.

David tapped the first column. “Strategic Fit. Strong. Their regulatory compliance practice overlaps almost perfectly with our core. Their commercial contracts work is adjacent. We could absorb it or refer it out. Their client base is mid-market Arizona and New Mexico, which is our target geography. Green.”

He moved to the second column. “Financial Performance. Solid. Revenue is $4.2 million, but it has been flat for five years. Margins are 22 percent, low because they are overstaffed relative to their revenue. They have eight associates doing work that our platform could handle with two or three lawyers manning the ship. No debt, but no growth either. Yellow.”

Third column. “Technology and AI Capability.” David circled the word he had written in red marker: Basically Zero. “They use Microsoft Word and a case management system from 2014. No AI. No automation. No data infrastructure. Everything we would need to integrate them onto our platform would have to be built from scratch. Red.”

Sarah took a sip of coffee. “People and Culture?”

“Mixed. But there is a surprise in here.” David had written two names and circled one. “Janet Hargrove is the key asset. Thirty years of client relationships, deep regulatory expertise, respected in the Tucson legal community. If we lose Janet, we lose the clients. She has indicated willingness to stay, but willingness in principle and willingness in practice are different things.” He paused. “The associates are the wildcard. Some of them might adapt. Some of them will be Joshua Thorntons.”

The name landed with weight. They both knew what it meant. Joshua Thornton had been Candor’s first bad hire, technically competent, culturally catastrophic. He had resisted every process David implemented, undermined Elena’s work, and nearly torpedoed the culture before Sarah finally let him go. One Joshua had been manageable. What happened when you absorbed an entire firm of people who had never worked alongside AI?

“Now the surprise.” David uncapped a blue marker and drew a circle on the whiteboard. “I pulled their client list and cross-referenced it with our target verticals. Seven of Janet’s twelve largest clients are mid-market pharmaceutical and biotech companies. Regulatory compliance work: FDA submissions, labeling reviews, manufacturing audits. The exact vertical we have been building since Cascade Biologics.”

Sarah set her coffee down. “Seven of twelve.”

“Seven of twelve. And her client retention rate is 94 percent over ten years. In a regional market, that is extraordinary.” David tapped the whiteboard with the marker. “This is the number that keeps me up on the other side. The client overlap is not just good. It is almost too good. If we absorb Janet’s book, we skip two years of business development in our strongest vertical.”

Sarah’s eyes settled on the blue circle on the whiteboard. The strategic logic was not hypothetical. It was sitting in Janet Hargrove’s filing cabinet.

“Regulatory Structure,” David continued. “Clean. Both firms are Arizona. No ABS complications for an intra-state acquisition. Standard bar notification requirements. Green.”

He reached the sixth column and set down the marker. “Integration Feasibility. This is the one that keeps me up.” He wrote the number fifteen, circled it, then wrote twelve next to it with an arrow pointing toward the first number. “We are fifteen people absorbing twelve. That is not a tuck-in acquisition. That is a merger. We would be doubling our headcount overnight. Our processes, our platform, our culture, everything we have spent three years building, would need to absorb an organization almost as large as we are. And we would need to do it while continuing to serve our existing clients and maintaining quality scores.”

The conference room was quiet except for the hum of the air conditioning.

Priya joined by video. She was at home, a Saturday morning, her laptop propped on a kitchen counter. Sarah had called her in because the technology integration question needed an engineering perspective.

“The technology integration is the easy part,” Priya said, studying the whiteboard through the camera. “Their case management data can be migrated. Their document repositories can be ingested into our pipeline. I would need a few months and one additional engineer, but the technical work is straightforward.”

“Then what is the hard part?” Sarah asked.

“The hard part is whether their lawyers can learn to work the way we work. Our pipeline requires structured inputs. It requires lawyers to review AI output, not generate original text. It requires trusting the system enough to let it do the first pass. That is not a technology problem. That is a human problem.”

David capped the marker. “That is the question Joshua answered for us. Some people can make the transition. Some cannot. And you do not always know which is which until you are in the middle of integration and it is too late to undo the deal.” But the key is the clients. It is far less important to determine how many of H & L’s team can cross the AI rubicon as to determine how many clients we can keep.

Sarah looked at the whiteboard. Six criteria. Two green, two yellow, two red, but one of the yellows now contained David’s blue circle, the client overlap that was almost too good. The overall assessment was amber, the most dangerous color, because amber invited rationalization in either direction. You could look at the greens and convince yourself the reds were manageable. You could look at the reds and convince yourself the greens were insufficient.

But amber was dangerous for another reason too: sometimes the green inside the amber was real. The client overlap was real. The vertical acceleration was real. And the Technology and Integration reds were just as real. Amber was the color of deals that closed because someone wanted them to close, not because the evidence necessarily demanded it, and it was also the color of deals that should have closed but didn’t, because someone was too cautious to see what was in front of them.

“Amber,” she said.

“Amber,” David agreed.

What History Shows

The Plumbing Behind the Deal

Three elements do most of the work in professional services combinations, and Sarah’s deal potentially touches all three.

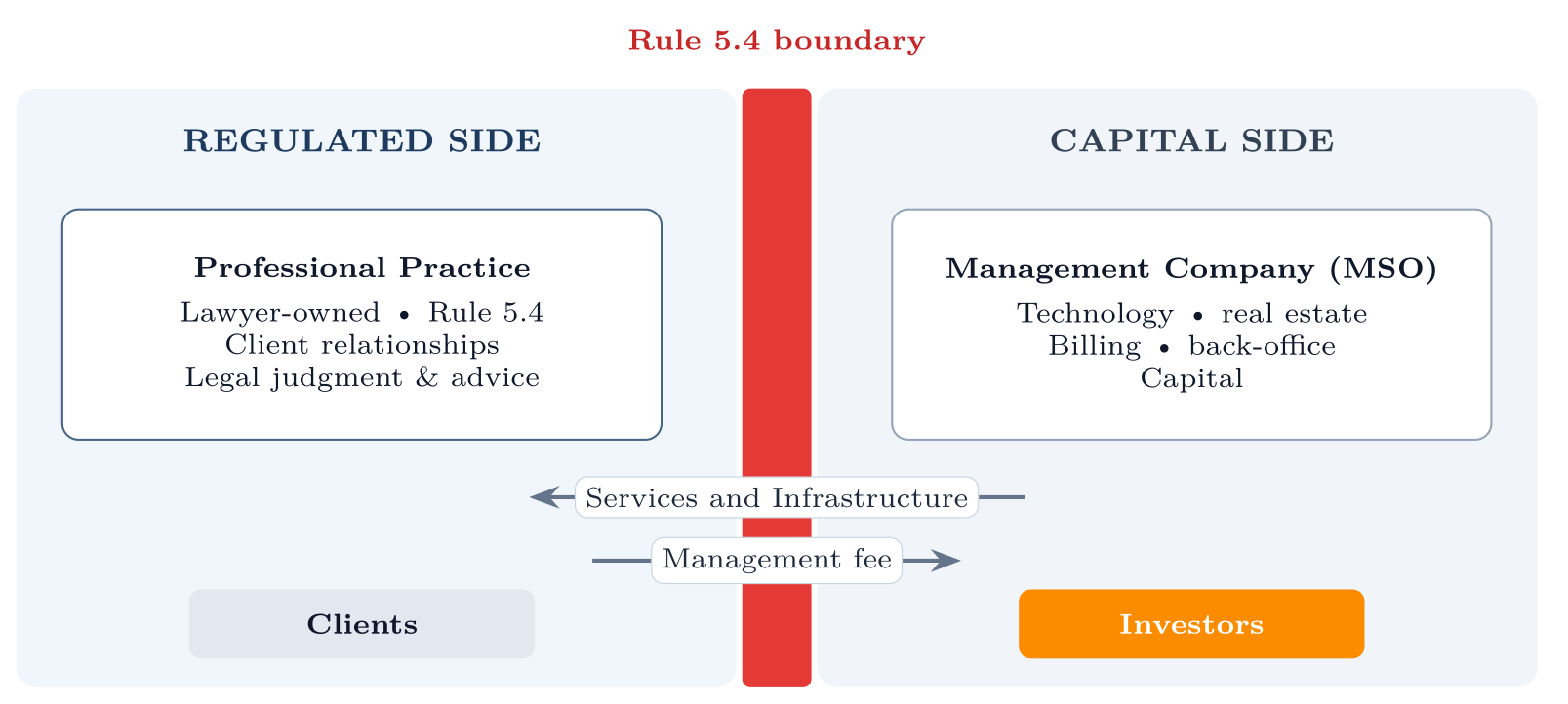

The Management Service Organization is the structure healthcare spent twenty years proving out and the one legal is now adopting on top of that precedent. The professional practice stays lawyer-owned and compliant under Rule 5.4 of the Model Rules of Professional Conduct. A separate management company provides technology, real estate, billing, and back-office services in exchange for a fee. Investors own the management company, not the firm. Industry reports of Big Law PE and MSO interest are likely to lead some to seriously explore such structures. Small to medium firms are perhaps even more likely to do so.

Earn-outs and rollover equity are the bridge structures that show up in almost every acquisition, and they are the ones sitting on Sarah’s desk this week. The Hargrove & Lyle deal as Alex framed it is $6.0 million in total consideration: $2 million in cash at close and a $4 million earn-out paid over twenty-four months against client retention. Retention is the primary trigger, not EBITDA, because retention is what Janet actually cares about. Her question on the call about “what happens to my people” was really a question about what happens to her clients, the nineteen-year pharmaceutical company in Tucson and the dozen others she could name without consulting a list, and the earn-out is structured so that the answer to her question is the same as the answer to Sarah’s. The sliding scale does the work: ninety percent retention or higher pays the full $4 million; eighty to eighty-nine percent pays roughly two-thirds; below eighty percent reduces the earn-out sharply and gives both sides a contractual reason to renegotiate the integration plan rather than litigate the gap. Janet’s incentives line up with Sarah’s from the moment the wire clears.

The headcount math is the final element. Not all twelve Hargrove lawyers stay. The two associates David’s due diligence flagged (the ones whose realization rates and supervisory dependence made them unlikely to adapt to the verification model) leave with severance at close. One of the retiring partners stays on through year one as an advisor to anchor the transition for the largest pharmaceutical accounts. The net combined entity, after the trim, is roughly fifteen Candor lawyers plus ten Hargrove lawyers (Janet, the second retiring partner’s continued half-time presence, and the eight associates targeted for retention) for an effective headcount near twenty-five (with an expectation that this combined headcount would likely further reduce due to voluntary attrition and further buyouts). The cross-sell potential is what really helps make the math of the deal pencil out. Tom Kaufman’s pharma network at Candor and Janet’s pharma network at Hargrove overlap in the biotech mid-market in ways neither side fully sees on its own. The combined firm has access to a vertical that Candor would have spent two years building from scratch, and Janet’s clients gain a verification layer and a fixed-fee model their incumbent firm could not have offered them. The Cascade Biologics engagement is the proof of concept for what that vertical looks like at scale. Hargrove brings the relationships, Candor brings the operating model, and the combined firm sells more to each side than either could have sold alone.

The structure cuts both ways. It reduces Sarah’s risk of overpaying for clients who walk after close. It also creates twenty-four months of operational entanglement in which the earn-out targets shape every decision Janet’s team makes, and twenty-four months of dispute surface area if the targets are missed.

What Happens When It Goes Wrong

The frameworks above describe how to evaluate paths and structure deals. But frameworks alone don’t prevent failure. The UK authorized Alternative Business Structures in 2011, giving us over a decade of real-world experience, including spectacular failures that show what the frameworks cannot fully capture. The UK’s Legal Services Act passed in 2007, with ABS approvals beginning in 2011, more than a decade before Arizona. Their experience provides essential lessons, particularly for combination strategies.

The board held a call the following week. Alex dialed in from an airport lounge; Margaret from her home office in Scottsdale; Rachel from the Juris Dictum conference room. Sarah and David sat side by side at the office, the whiteboard evaluation still visible behind them.

Sarah had planned to present the Hargrove & Lyle assessment, but Margaret spoke first.

“Before I raise concerns, and I will raise concerns, I want to acknowledge that the strategic logic here is genuine. The regulatory overlap is real. Janet Hargrove’s practice is exactly the kind of adjacent capability that makes combination strategies work when they work. I have seen it succeed.” A pause. “I have also seen it fail. Spectacularly.”

She adjusted her reading glasses. “So let me make sure everyone in this room understands the base rate for professional services acquisitions.” Margaret’s voice carried the particular authority of someone who had watched deals go wrong from the inside. “Axiom Ince grew entirely by buying up smaller, distressed firms. Then it imploded. I was not on the inside, but the most generous characterization I could offer is that the controls never caught up with the headcount.”

“That is an extreme example,” Alex said.

“All failures are extreme in retrospect. At the time, they looked like ambition.” Margaret paused. “What about SSB Law? A volume consumer-claims shop, collapsed a few years ago owing lots of money and with a stack of complaints to the regulator.”

Another pause, the reading glasses coming off this time. “The list goes on. Slater and Gordon. Australian firm, publicly listed, the model everyone in our industry was supposed to admire more than a decade ago. It acquired aggressively in the UK and took it on the chin. The firm survived, eventually went private again, but the lesson is the one that matters. Acquisition-led growth is a minefield, so be careful.”

Rachel spoke from the screen. “Margaret, are you saying we should not pursue this?”

“I am saying that the question is not whether the target is attractive. The question is whether you can integrate faster than complexity compounds. Every acquisition adds complexity. Complexity compounds. If your integration capacity is linear and complexity growth is exponential, there is a crossover point, and beyond it, you can lose control.”

The room was quiet. Her gaze drifted to the whiteboard behind her. Amber.

Alex was ready to chime in. “The UK has a ton of ABS firms in operation. Collectively, they occupy a real slice of the overall market. They introduce new services and adopt new technology at roughly twice the rate of traditional firms, and private equity has flowed in over the past years. The failures Margaret named are not the typical case. They are, however, the instructive case, and what they share is more important than what distinguishes them. Each firm scaled through acquisition faster than its compliance infrastructure could keep up. Each kept growing past the point at which its monitoring systems could see what was actually happening inside the new business. And in each, the pressure that drove the next acquisition was the same pressure that overrode the discipline to integrate the last one. This needs to be done with care.”

What Happens When It Goes Right

Failure is not inevitable. Healthcare has operated under restrictions parallel to MRPC Rule 5.4 (corporate practice of medicine and dentistry prohibitions that, in many U.S. states, bar anyone other than licensed physicians and dentists from owning clinical practices) but has developed combine-path models at a scale legal has not yet approached. Two firms in particular sit behind the legal MSO thesis: Heartland Dental and Aspen Dental Management.

Heartland Dental was founded in 1997 by Dr. Rick Workman, a practicing dentist in Effingham, Illinois, who built a management company alongside his own clinic to handle the parts of running a dental practice that had nothing to do with treating patients. The clinical practices stayed dentist-owned. The management company handled real estate, technology, billing, hiring, and capital. By 2018 the structure was attractive enough that KKR took a position, and the platform supports roughly 1,800 affiliated offices today. The discipline that distinguishes Heartland from the UK accumulators is the same one David is testing for with his Integration Feasibility column: the boundary between clinical decisions (dentist) and business decisions (MSO) is held as a constitutional matter, not a preference that bends when growth pressure builds.

Aspen Dental Management followed a similar arc on a slightly later timeline. Robert Fontana founded it in 1998. American Securities led a recapitalization in 2015, with Leonard Green & Partners among the backers. The branded network now exceeds 1,000 offices. Aspen also offers the cautionary half of the precedent: the company has faced regulatory scrutiny in several states for whether the management company strayed across the boundary into clinical control, the same boundary-of-practice question the legal MSO structure will face. The lesson the two firms together teach is not that the MSO model is safe. The lesson is that the model can scale when the regulated activity is genuinely kept inside the regulated entity, and that the failure mode is always the same: the management company, under capital pressure, reaches across the line. Legal MSO operators will inherit much of the same precedent, the temptation and opportunity that MSO operators in the medical field faced in earlier decades.

The Decision

Hargrove & Lyle was the opportunity sitting on Sarah’s desk that Thursday evening. It was decision time. The cleaning crew had come and gone. The building was empty except for her and the hum of the server closet down the hall. The dashboard glowed on her monitor, the numbers still green, still strong, still the best Candor had ever posted. Behind her, David’s whiteboard evaluation was still visible through the glass wall of the conference room. Six columns. Two green, two yellow, two red. Amber.

She had spent the week reading everything she could find on professional services acquisitions. The UK ABS failures. The healthcare MSO successes. The academic literature on post-merger integration, most of which boiled down to a single finding: most acquisitions destroy value, and the acquirer’s confidence in their ability to beat the base rate is itself a risk factor.

She had talked to Janet Hargrove by phone, a cautious, but much deeper conversation than their original interaction arranged through Alex’s PE contact. The call had lasted more than two hours. Sarah had expected polite evasion. What she got was a woman who spoke about her practice with the specificity of someone who had earned every client the hard way.

“I have a pharmaceutical research company in Tucson that I have represented for nineteen years,” Janet said. “Started with their first FDA submission when they were twelve people in a strip-mall office. I know their general counsel’s wife’s name. I know their CFO’s daughter’s college plans. That is not a relationship you can migrate onto a platform.”

“I understand that,” Sarah said. “We would not try to replace what you do. The question is whether there is a way to support it.”

“Maybe. I am getting to that.” Janet’s voice was direct but not hostile. “Carl and Dennis checked out three years ago. They come in at ten, leave at four, and the clients know it. I am carrying this firm on my back, and I am fifty-eight years old, and I would like to stop carrying it before I am sixty-five.”

“What do you want to happen?”

“I want the clients to be taken care of. That is not a platitude. I mean it literally. I have pharmaceutical companies that depend on us for compliance work that keeps their products on the market. If this firm goes dark because Carl and Dennis retire and I cannot sustain it alone, those clients suffer.” A pause. “I have read about what firms like yours are doing. I do not understand half of it. But I am not afraid of it. I am afraid of retiring partners and a firm that goes dark six months after I hand over the keys.”

Sarah listened, and something turned over in her chest. Janet reminded her of the best partners at her old firm, the ones who did excellent work and were quietly terrified of change, not because they lacked courage but because they understood what change could cost.

Sarah found herself wanting to say yes. She found herself wanting to tell Janet that Candor could be the answer, that the platform and the people and the culture she had built were exactly what Hargrove & Lyle needed. She did not say it. But the wanting was there, and she noted it with the clinical attention of someone who had learned to distrust her own enthusiasm.

Sarah picked up her phone and called Alex.

“I have a decision,” she said.

“I am listening.”

“Not now.”

A pause. “Tell me why.”

“Three reasons.” She looked at the whiteboard through the glass. “First, we are fifteen people. Absorbing twelve is not an acquisition—it is a merger. We do not have the integration capacity. David is already running operations, finance, and half the client relationships. Priya’s team is building platform features for our existing clients. There is no one to run an integration. I would have to do it, and if I do it, I am not running the firm.”

“You could hire an integration lead.”

“With what money? We have not raised the Series A. The acquisition itself would cost $4 to $5 million. The integration would cost another million in consulting, technology migration, and the inevitable fires. That is $6 million we do not have, for a firm whose value depends entirely on client relationships that might not survive the transition.”

“What is the second reason?”

“Timing. We have not raised the Series A yet. Our margins are trending in the right direction but we are not yet at the scale where we can absorb a setback. If the integration goes badly, if we lose Janet’s clients, if the associates revolt, if the technology migration takes twice as long as Priya estimates, we do not have the runway to recover. We would be betting the firm on an acquisition when the firm itself is still proving its model.”

Alex was quiet.

“Third reason is cultural risk. We lost Joshua Thornton, one person, and it nearly broke us. We would be absorbing eight associates who have never worked with AI, never followed a standardized process, never had their output reviewed by a correction pipeline. Some of them will adapt. Some will not. And the ones who do not will poison the culture the same way Joshua did, except there will be more of them and they will have each other for reinforcement. But mostly I do not think Janet fully appreciates the nature of her situation and I fear she will (intentionally or unintentionally) undermine this. I think if we come back later she might be more amenable.”

“So it is a no.”

“It is a not now.” Sarah pulled the legal pad toward her. “Keep the relationship warm with Janet Hargrove. If we raise the Series A and build an integration playbook, hire someone whose job is to plan and execute acquisitions, then Hargrove and Lyle, or someone like them, could be a Year Three play. Build first. Build the infrastructure to combine. Then combine.”

The line was quiet for a long moment. When Alex spoke, his voice was measured, the voice of a man conceding a point he did not fully want to concede.

“I hear you. And your reasoning is sound, all three points.” A pause. “I still think you could pull it off. I have seen founders absorb firms this size and come out stronger. But I trust your read on the team’s capacity more than my own. You are closer to it. I guess walking away might give them a great dose of reality. Or you might lose them forever but I understand you are prepared to take that risk.”

Sarah felt relief, but it came threaded with the weight of having disagreed with her lead investor. Alex had not built his track record by being wrong about growth timing. The possibility that she was the one making the mistake sat in her chest like a stone she would carry for a while.

“All right. Not now. But Sarah, keep the relationship warm with Janet. If the conditions change, I want us to be first in line.”

“I will.”

After they hung up, Sarah sat in the quiet office. The relief did not settle the way she had expected it to. She had won the argument, and Alex had yielded gracefully, and the firm would stay on the build path. But Alex still believed in the deal. He had not been testing her. He had been persuaded (partially, reluctantly) and the distance between his conviction and hers was a space she would have to live inside for a while.

Janet Hargrove’s voice echoed in the quiet: the pharmaceutical company in Tucson, nineteen years, the firm going dark. Sarah found herself rehearsing the argument she would have made for the deal. The client overlap: seven of twelve. The vertical acceleration. David’s blue circle on the whiteboard, the number that was almost too good.

She reached for her phone and texted David: Decision is no. Not now. Will explain Monday.

His reply came two minutes later. Three words and a period: Understood. See you Monday.

Sarah stared at the screen. She knew David well enough to hear the weight in the brevity. He had spent his Saturday on that whiteboard. He had uncovered the client overlap, mapped the vertical fit, scored six criteria in his precise block lettering. He did not argue with the decision. But the Moleskine was full of analysis that would never become action, and David Park was not a man who wasted analysis lightly.

She picked up her pen and wrote on the legal pad, below the three columns she had drawn that Friday morning (Build, Transform, Combine), a single line in her own handwriting:

The right path at the wrong time is the wrong path.

She turned off the monitor, picked up her bag, and drove aimlessly through the vast Phoenix streets. Somewhere on Camelback Road, she caught herself rehearsing the pitch she would have made to Janet. The one where she said yes. The one where she told Janet that Candor could be the answer, that Candor OS 2.0 and the people were ready, that the nineteen-year pharmaceutical client would be in good hands. She shook it off. The discipline had held. But discipline, she was learning, did not come for free. Even the right decision at the right time can still feel half wrong.